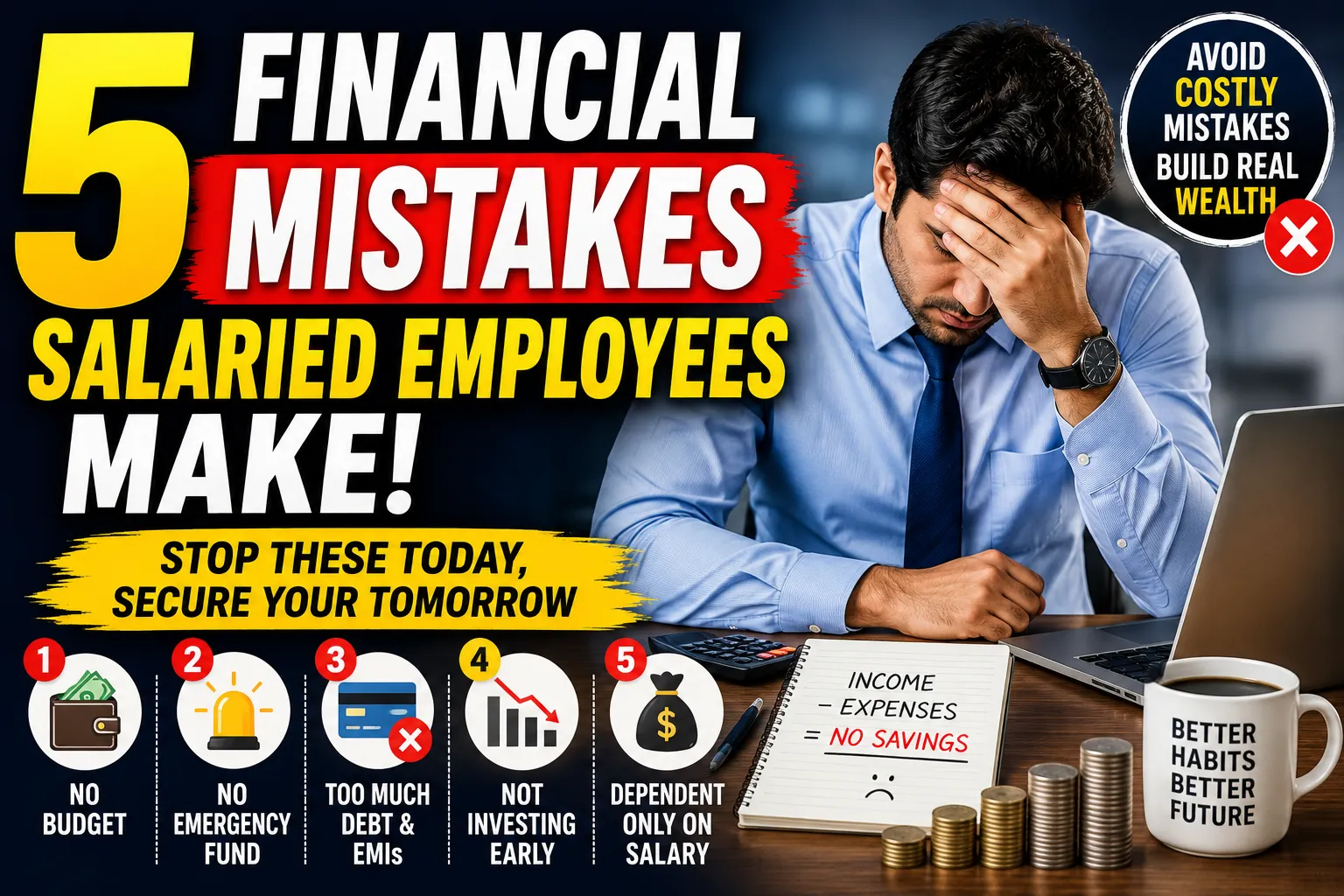

Most salaried employees feel financially secure — after all, a fixed income hits the account every month, and that sense of predictability can feel like enough. But here’s the uncomfortable truth: a steady salary is just the starting point. What you do with that money every single month determines whether you’ll be financially free at 50 or still working at 70 because you have no choice. After years of watching people earn well but save poorly, the same five mistakes keep showing up again and again. Let’s talk about them honestly.

Mistake 1: Treating Savings as Whatever Is Left at the End of the Month

This is the most common and most damaging mistake of them all. The typical salaried employee gets paid, pays bills, spends on lifestyle, enjoys a few weekends out, and then saves whatever is left — which is usually very little, sometimes nothing, and occasionally negative. The month just somehow slips away.

The fix is simple but requires a mindset shift: pay yourself first. The moment your salary hits your account, move a fixed amount to savings or investments before you do anything else. Set up an automatic SIP on the 1st or 2nd of every month so the money moves before your brain can decide it needs new shoes or a dinner out. Over time, you naturally adjust your lifestyle to whatever remains — and this one habit alone can transform your finances completely. Even ₹5,000 a month invested consistently in a decent equity mutual fund for 20 years can grow to something that genuinely changes your retirement picture.

Mistake 2: Confusing Insurance with Investment

This one has cost millions of Indians lakhs of rupees, and it continues to happen because of how aggressively certain products are sold. A well-meaning uncle, a bank relationship manager, or an LIC agent convinces a fresh employee to buy an endowment plan or a ULIP that “gives returns and also covers your life.” It sounds perfect. It is not.

Traditional insurance-cum-investment plans typically give you 4–5% returns over 15–20 years, which barely beats inflation. Meanwhile, your life cover is laughably insufficient — often just 5–10 times your annual premium, which translates to a cover of ₹3–5 lakh when your family actually needs ₹1 crore or more to sustain themselves if you’re gone. The right approach is to keep these two things completely separate. Buy a pure term insurance plan — ₹1 crore cover for a 30-year-old costs roughly ₹8,000–10,000 per year. Invest the rest in mutual funds or index funds. You’ll end up with better protection and dramatically better wealth creation. If you already own one of these bundled plans, do the math honestly and consider surrendering if it makes sense.

Mistake 3: Ignoring Tax Planning Until February or March

Every year, the same panic. It’s February, HR sends a reminder about investment proof submission, and the salaried employee scrambles to dump money somewhere — anywhere — just to save tax. ELSS funds get bought in a rush, PPF deposits get made without thought, and insurance premiums get paid for policies that perhaps shouldn’t have been bought in the first place.

Tax planning is not a February activity. It is a full-year strategy. When you plan from April itself, you can actually choose where your Section 80C ₹1.5 lakh goes intelligently — ELSS for wealth creation, PPF for stable long-term debt, home loan principal repayment if applicable. You can also explore Section 80D for health insurance premiums, NPS for an additional ₹50,000 deduction under 80CCD(1B), and HRA calculations if you’re renting. Proactive tax planning done right can legally save you ₹50,000 to ₹1,50,000 in taxes every year depending on your income slab — money that can then be invested instead of handed to the government unnecessarily.

Mistake 4: Having No Emergency Fund and Funding Emergencies with Credit Cards or Loans

Life does not care about your salary credit date. The car breaks down, a family member needs hospitalization, the landlord demands a sudden deposit, or — and this one became very real for many people — you lose your job without warning. What happens then? For most salaried employees with no emergency fund, the answer is a credit card swipe, a personal loan, or an embarrassing call to a family member.

A credit card used in a crisis and not paid in full becomes a debt spiral very quickly. Personal loans from banks or apps carry interest rates of 12–24%, and suddenly your financial life is going backwards despite your income. The rule is straightforward: build an emergency fund of 3–6 months of your total monthly expenses and park it somewhere liquid — a high-interest savings account or a liquid mutual fund works perfectly. This money is not for vacation. It is not for a sale. It sits there and does nothing until the day it does everything. Building it takes time, but start with a goal of ₹10,000, then ₹25,000, then work your way up. Even a partial emergency fund changes how you handle a crisis.

Mistake 5: Lifestyle Inflation That Perfectly Matches Every Salary Hike

You get a 20% hike. Wonderful. Within three months, you’ve moved to a bigger flat, upgraded your phone, started eating at better restaurants, and your EMIs have grown to match. Net savings? Roughly the same as before the hike. This pattern repeats with every promotion, every increment, every bonus — and it is called lifestyle inflation, and it is the silent killer of wealth.

The problem isn’t enjoying your money. You absolutely should enjoy the fruits of your hard work. The problem is when 100% of every raise goes toward a bigger lifestyle and 0% goes toward a bigger future. A much healthier approach is the 50-50 rule for increments: whenever you get a raise, let 50% of that extra money improve your lifestyle and direct the other 50% straight to investments. You still live better, but you also build wealth faster. Bonuses deserve the same treatment. Getting ₹1 lakh as a Diwali bonus and spending the full thing feels great for a weekend — investing half of it feels great for the next 20 years.

The Bigger Picture

None of these mistakes happen because salaried employees are careless or unintelligent. They happen because nobody teaches personal finance in school, because financial products are sold rather than explained, and because lifestyle pressure is real and constant. The good news is that awareness alone puts you ahead of most people. You don’t need a massive salary to build serious wealth — you need consistency, a little discipline, and the willingness to make slightly better decisions month after month. Start with one fix from this list today. Just one. That is genuinely enough to begin.